The British decision to veto the proposed new EU treaty is not surprisingly provoking an avalanche of commentary this weekend. Among journalists, at least, there seems to be a consensus that David Cameron committed

some kind of major diplomatic blunder.

Possibly this is so, but given the difficulties presented by having to take this agreement forward outside the formal structure of the EU, it is hard to not reach the conclusion that both Angela Merkel and Nicolas Sarkozy have been guilty if not of a similar blunder, then at least a major error of judgement. On the other hand the issues involved in the proposed new arrangements are highly complex and in some senses ground breaking, so it is indeed suprprising that so many (and so diverse) countries were able to reach such rapid agreement on the need for and the broad outlines of a new agreement. While Angela Merkel was probably worried before the meeting that too few countries would sign up (there was talk of only a hard core of countries proceeding), now she is surely concerned by the fact that so many have. In many ways the biggest weakness of her debt brake proposal is that it has become "too successful" to be fully credible.

A Continent Which Has Isolated Itself From The British Isles?

That British "separatism" has again raised its ugly head should not be surprising, since this issue has a long history (as I was only too clearly reminded yesterday when the local TV news here in Catalonia ran footage of

General de Gaulle warning that allowing the UK to enter the common market would be a major strategic mistake and a significant setback for the European construction process), but the water in which all this discourse flows is now so mirky that it is hard to separate what is really relevant to the point at issue, and what isn't.

In fact France, Germany and the UK should have reached agreement before the summit even started, and the agreement should have been restricted to measures which were considered necessary to resolving the Euro debt crisis, including the rules and institutions which are lacking. Maybe it is a pity that these three countries have to have such a decisive role in European decision making, but for better or worse that is the way it is.

Now the UK has exercised its veto, and we have a legal mess. According to

Peter Spiegel writing in the Financial Times, Britain’s rejection of treaty changes means that the other 26 EU members will now have to jerry-rig an intergovernmental system without the automatic right to use the EU’s institutions, leaving decisions taken vulnerable to continuing legal challenge. As a result financial market participants will have one more reason to doubt the new fiscal pact’s viability and credibility.

"The arcane issue of whether a group of countries acting outside the EU’s treaties can use the European Commission, with its surveillance and enforcement powers, and the European Court of Justice, has been pushed to the forefront of the eurozone debt crisis. Britain, which refused to sign up to a treaty, but does not wish to see itself sidelined altogether, insists that its 26 EU partners must do without the European institutions".

If the European Union's institutional maze

was already proving hard for investors and external policy makers to follow, this latest twist in events will hardly make it easier for them.

This is an outcome that should have been avoided at all costs, and indeed I think the most intelligent thing the three of them could do now would be to meet again and find a solution to the real problem at hand before the euro finally blows itself apart, with highly undesireable consequences for all of us.

People say that the EU was created to ensure there were no more wars in Europe but personally I think a West European centred WWIII was never a very likely eventuality. In any event the EU could have been set up with a much more limited objective, namely to end periodic outbreaks of tribalism and jingoisim. This is the real European curse, and this is what we are now facing in one country after another, as - with the local national press in the vanguard - each blames the other for causing the crisis, or for not reaching the much needed agreement to end it. The sad reality is that Europe's leaders fiddle even as Rome is about to burn.

Save The Euro!

The nub of the question is the Euro, and setting up some form of workable common governance for those countries who belong to the monetary union. In this sense an agreement between the 17 countries who share the common currency would have made perfect sense, and in is not clear to me at least why the UK (or countries like Bulgaria and Romania for that matter) would need to be party to this kind of agreement. But, it seems, representatives of the EU Commission and the German and French governments have been so concerned to identifty saving the Euro with the idea of saving Europe that this important point of detail seems to have gotten buried well down in the pile of paperwork.

Countries like the UK, Sweden and Denmark do not use the Euro since they decided not to do so. Countries like Latvia and Lithuania do not use it since they were not allowed to, and the EU even refused a 2008 request from the IMF to allow Latvia to devalue and enter the currency area at a moment when that country was indeed in a situation of most urgent need.

What the latest tiff underlines more than anything else is the way we are lacking a coherent and consistent account of what the relationship between the EU and the Euro is, and this is not something which has only been discovered yesterday. Maybe the seeds of what happened last Friday are the result of having the Euro regulations form part of the EU Treaty itself, rather than being an agreement between a more limited group of countries in the manner that is now being proposed. Again, if the Euro was to form one of the indispensible parts of the EU Treaty, in many ways it didn't make sense to allow the East European members to join until the had fulfilled the Maastricht criteria for Euro membership.

Viewed in this light, last Friday's events were always a problem which was waiting to happen.

It may well be that the Euro was created as a stepping stone towards a form of political union that not all member countries wanted, but now we are apparently seeing a sort of fait accompli shotgun wedding, since without such an enhanced union, not only may the currency itslef fall apart, but entire global financial system, and everything we know and love seems likely to be carried away with it. I'm not sure whether or not this constitutes moral hazard, but it sure as hell constitutes a pretty potent form of moral blackmail.

Fiscal Pact or Fiscal Union?

Then again, what Europe's leaders were talking about last Friday was not just any old kind of political union. Despite all the talk about creating the groundwork for fiscal union (it will be remembered that one of the commonly cited differences between the dollar and the euro as common currencies is that all states in the American Union are backed by the US Treasury, while the world still waits to learn who - or what -

is backing the individual states in the European one). What we we are being offered is not a common treasury of the kind which would convince markets that there was something solid standing behind the currency, but rather what

Wolfgang Munchau recently referred to as "another one of those Silly growth and Stability Pacts".

"Contrary to what is being reported, Ms Merkel is not proposing a fiscal union. She is proposing an austerity club, a stability pact on steroids. The goal is to enforce life-long austerity, with balanced budget rules enshrined in every national constitution. She also proposes automatic sanctions with a judicially administered regime of compliance".

Doing The Berlin Brake Dance

What Wolfgang is getting at here is that the core of the proposed EU agreement is the introduction of the so called "balanced budget amendment" as a binding principle across all the eventual signitaries. Naturally Germany already has this amendment in place.

According to Wikipedia: "In 2009 Germany's constitution was amended to introduce the Schuldenbremse ("debt brake"), a balanced budget provision. This will apply to both the federal government and the Länder (states). From 2016 onwards the federal government will be forbidden to run a deficit of more than 0.35% of GDP. From 2020, the states will not be permitted to run any deficit at all. The Basic Law permits an exception to be made for emergencies such as a natural disaster or severe economic crisis".

This is the role model for the kind of constitutional amendment other states will now be expected to introduce -

as the Economist wryly notes perhaps Schuldenbremse will one day form part of the French and Italian languages in the same way “kindergarten” has become part of the English one.

The 0.35% deficit permitted is in fact a form of what is termed "structural deficit", that is to say there is a formula according to which it can be averaged out over the economic cycle, although even after allowing for this the deficit number is not going to be that high, and in any event at no point should the deficit exceed 3% of GDP.

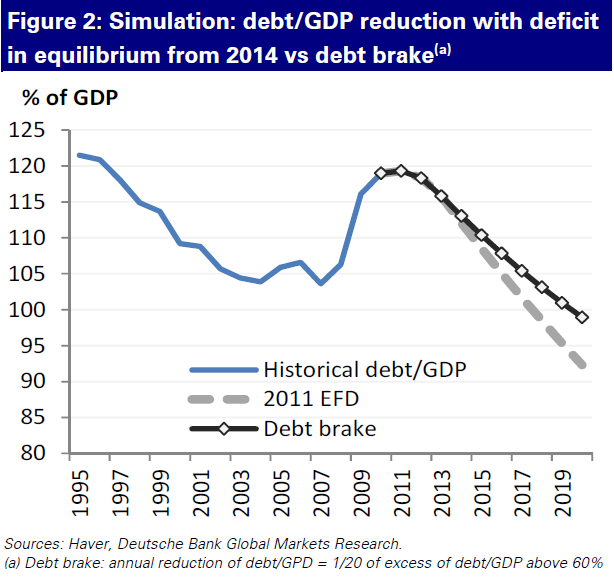

More important even than this deficit restriction, however, is the so called debt brake principle, which implies countries must steadily reduce their debt to 60% of GDP over a specified time period. If, as may be anticipated, growth and inflation in the Euro Area is going to be low, then effectively countries will not be running deficits at all, but rather surpluses, depending on how much over 60% they will be when the present crisis comes to an end, and what the time scale for reduction eventually is. As far as I can see the current proposal for the new pact coming from the finance ministers (Ecofin) is that from 2013 countries reduce the part of the debt which is over 60% of GDP by 1/20 per annum.

At the end of the day one thing is clear, and this has not been emphasised enough in the press reporting of the summit, this is the end of Keynesian demand management as a policy tool as it has been practised in Europe since the end of WWII. That is to say, while it is be one thing to argue that simply creating more debt through fiscal policy may not be the most appropriate way to solve a crisis which has been caused by excessive indebtedness, it is going a bridge further to suggest that counter cyclical fiscal policy should not be practised. Germany's leaders have, it seems, crossed that bridge. Naturally not all German economists agree. As

the Economist reports Peter Bofinger, one of five economic “wise men” who advise the German government, is one of them. On a normal Keynesian view, the balanced budget ammendment could choke-off economic recoveries - some would argue Germany's commitment to this principle at this point is an example of this issue. Having a structural component in the target target allows deficits to rise slightly when output falls below trend with the additional deficit being offset by surpluses during upswings. But, as Bofinger argues, this “assumes textbook-like economic cycles,” and garden variety recession. In the real world cycles and crises vary. An externally induced recession followed by a weak recovery can excessively reduce potential growth, while the balanced budget restriction would restrict the deficit spending needed to stimulate demand.

Given the magnitude of these issues, it is surprising how little debate the proposal is generating, and of course it is hard not to be struck by how quickly people who obviously would not have understood what was really involved were to arrive in Brussels and offer to sign on the ditted line without too much attention to the small print. The exact detailing of the amendment varies - in Spain for example the limit is 0.4% of GDP for the deficit, and the limit is operationalised in 2020. In addition the Spanish wording is also interestingly different from the German version, since it stipulates that the limit can only be exceeded in the event of "natural disaster, economic recession or other extraordinary circumstances". This substitutes the wording "economic recession" for the German "severe economic crisis" variant, which really rather than concealing any sinister intention suggests to me more than anything that the Spanish parliament didn't understand what they were voting for, since the idea is (as I say) for structural deficit over the cycle, and "cycle" obviously includes recession, so a mere recession cannot be an exception, though what counts as "severe" in the German case doubtless awaits interpreting in the courts.

Here Comes My Nineteenth Nervous Brake-down

Once more the Economist gets the basic point:

"Germany has yet to put its debt brake to the test. The federal government made things easier for itself by a generous calculation of last year’s structural deficit, which is to be cut in equal annual steps to reach the 2016 target. Flush with cash, thanks to a strong economy, it has found room for giveaways to voters without falling foul of the brake. Civil servants will get a bigger Christmas bonus next year, for example. For the Länder, the 2020 deadline seems a long way off: 13 of them budgeted for increases in structural deficits this year, laments a study by RWI Essen, a research institute. A “stability council”, composed of federal and state ministers, has little power to sanction prodigals. Apparently, it is as toothless as the enforcers of European financial discipline".

There is an imbalance in voting intentions between countries. Angela Merkel is marking out a very long term agenda:"This is a breakthrough to a union of stability,"

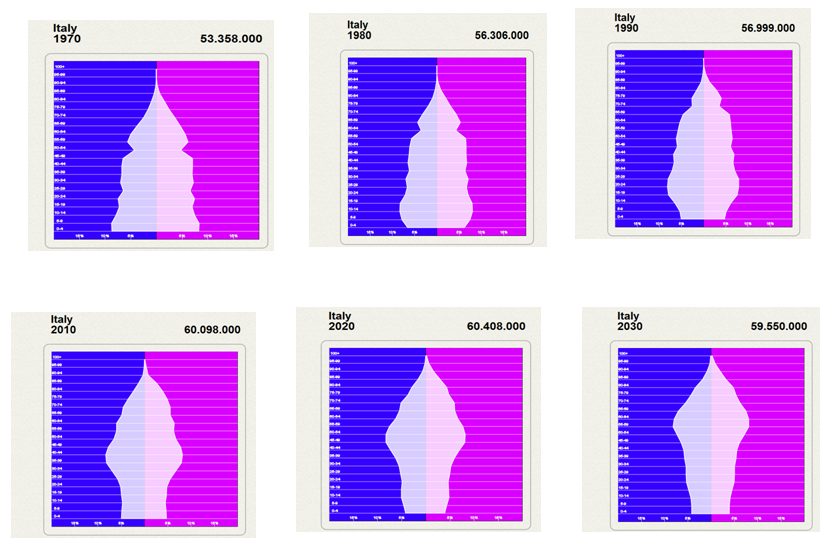

Reuters cite her as saying. "We will use the crisis as a chance for a new beginning." It is hard to see why countries like Romania and Bulgaria with a very poor institutional record are in such a hurry to sign up to this without a lot more reflection. The use of the word "stability" is very important. Merkel is prioritising sustainability and stability in the longer run over short term growth. This is very consistent with a whole German view of things and completely in harmony with the ecological strain of thought in the modern German world view. I have a lot of respect for this (even where I disagree), and especially for the fact that someone in Europe is trying to think in the longer term. But I cannot help feeling many of the people and countries voting for the new agreement were only thinking about their financing needs in the short term, and were not fully cognisant of the fact that they were voting for a new beginining, a new type of Europe, where living standards may be lower, but the debt dynamics will be more stable. Personally I can only make sense of this in terms of Europe's current demographics, and the challenge that is represented by maintaining health and pension systems in the face of low growth and ageing and declining workforces.

Each Unhappy Family Is Unhappy In Its Own Way

Hence perhaps the most worrying thing about last weeks agreement to agree was that each and every one of the 26 countries concerned has stated that "I will stop beating my wife, I promise I will, and soon", but understands what this means in their own special way. Despite the fact that Germany has been quite clear, for example, the much respected

Mario Monti is sure that Euro Bonds are almost within reach.

"Italian Prime Minister Mario Monti said Germany and other countries will eventually be convinced that commonly issued euro zone bonds are a useful way of tackling the region's debt crisis. "I believe we have enough arguments to convince the Germans," Monti told Euronews in a television interview". He also is still pushing to have the funding capacity of the EFSF increased, again as if the German parliament had not voted to put a ceiling on the level of its exposure. "Monti said he regretted that European leaders had not agreed to increase the European bailout fund (EFSF) by more than 500 billion euros ($668.25 billion) at last week's meeting in Brussels. A more substantial firewall would have been a better guarantee against market tensions, he said, adding this had been blocked by several European countries that "have a very limited view of what is the common interest".

The worrying thing is not only that Mario Monti believes this but, more importantly, that this is probably what he is telling the Italian electorate, leaving them with a very limited understanding of the kind of sacrifices they are actually going to be ask to accept. Last week's round of 2012 austerity measures will be as nothing when compared with those that would really be required to get Italian debt back down to 60% of GDP.

Thus many of those who were eagerly struggling to be first to sign on the dotted line last Friday didn't get the gist of the point of what they were signing up to, and the agreement will only really be adding to credibility once it is tried and tested. In the meantime everyone is simply following the lead given by Mario Monti, and assuming that what is actually going on isn't the death of Keynes, but the birth of German funded Eurobonds.

Land Ahoy!

But, having said all this, let's go back to where we started, to the isolation of the UK within the European Union. Could it be,

as Philip Stevens suggests in an opinion piece in the Financial Times, that the UK is on its way out of the EU? As he says, it all depends on which end of the telescope you look down. Viewed from one one end, Mr Cameron’s veto was the moment Britain signalled the beginning of a long goodbye to Europe; looked at through the other it was Europe bidding its farewell to Britain. But are we sure, even Stephens has his doubts:

"It is important to insert a caveat here. The presumption of everyone in the room in Brussels was that the eurozone countries will indeed succeed in saving the single currency and build alongside it a more integrated political union. That enterprise could yet fail. Some will say after the limited progress made at the summit on rescue plan, the odds have now stacked against the euro. If it were to fall apart, so too would all other ambitions among the 17 eurogroup members".

So advertently or inadvertently David Cameron now has a Euro put. If the Euro survives his fate is sealed, in the most negative of senses, yet if it fails, then not only will he have been proved right, he may also find himself having to assume the mantle of leadership (backbench eurosceptics and all) and instill in a European Union in complete disorder the kind of Dunkirk Spirit for which the islands from which he hails have made themselves famous. And while we are on the question of survival, perhaps it would be to the point to close with

John Authers assesment of the state of play in the argument.

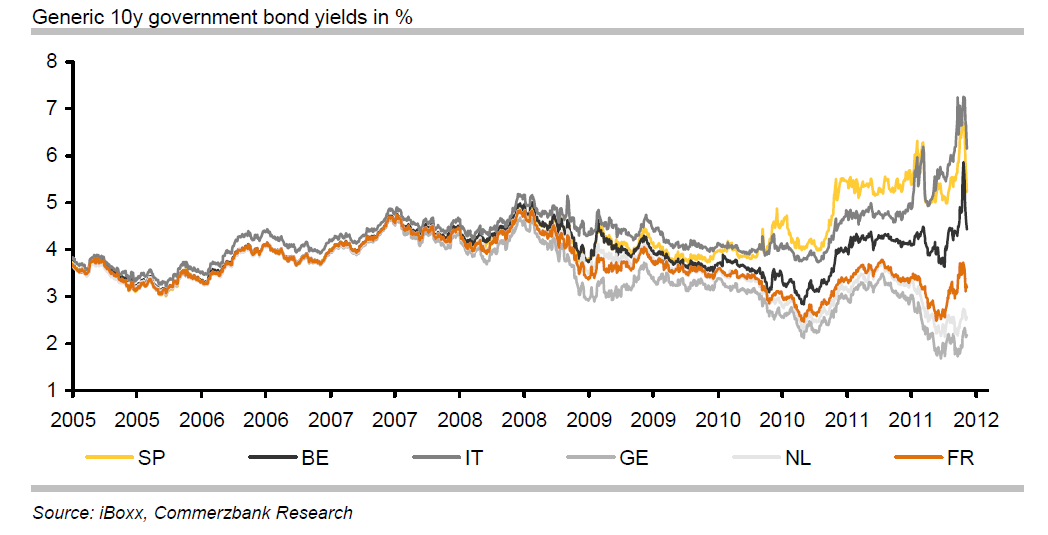

Amid all the heated speculation about the European Union summit’s impact on Europe’s economic future and Britain’s role in it, traders are asking a more mundane question: “Has it done enough to get us through to Christmas?” Their answer: probably not. The muted market moves on Friday may be misleading. The euro rose against the dollar – but this may have been driven by banks repatriating assets. European bank shares, while above their lows, trade at half their book value, implying grave fears that some of their assets will be written down. The yield on Italy’s 10-year government bond fell 30 basis points during the day to 6.32 per cent – but this is still higher than at any point in the eurozone’s history until a month ago. The risk remains that the market will test Mr Draghi’s resolve by attacking a peripheral country’s debt in the two weeks before Christmas – particularly if a rating agency provides an excuse.

Amen to that! This post first appeared on my Roubini Global Economonitor Blog "

Don't Shoot The Messenger".